This week’s market tone is defined by surging crypto ETF flows, revived trade uncertainty, and growing anticipation for Friday’s U.S. inflation data. Here’s what’s moving the markets.

Crypto ETFs: Momentum Is Back

Institutional demand roared back into crypto-linked ETFs to start the week.

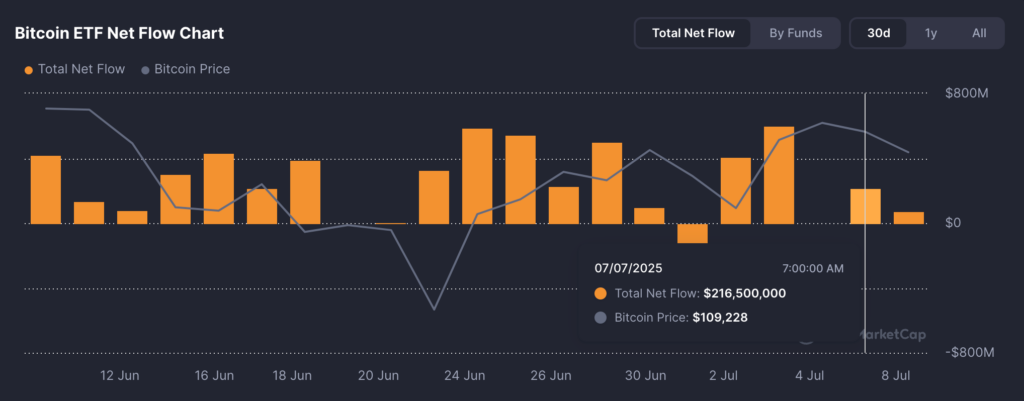

Bitcoin ETFs attracted $216.64 million in net inflows, with BlackRock’s IBIT leading the charge at $164.64M, followed by Fidelity’s FBTC with $66.05M. Despite small outflows from GBTC and ARKB, overall sentiment was strongly bullish. Daily trading volume for Bitcoin-linked ETFs hit $2.89 billion, pushing total net assets to $135.71 billion.

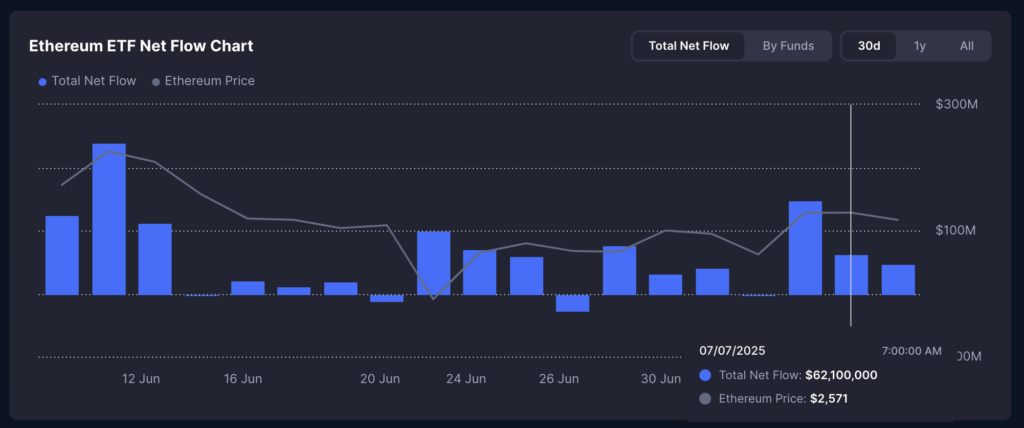

Meanwhile, Ethereum ETFs also saw a sharp uptick, bringing in $62.11 million. BlackRock’s ETHA accounted for $53.21M, while Fidelity’s FETH added $8.9M. With no recorded outflows, Ether funds continued their eight-week green streak. Total ETH ETF assets climbed to $10.71 billion, with nearly $400 million in daily turnover.

These flows signal more than a speculative bounce—they show rising conviction that crypto is becoming a mainstream portfolio component, especially as macro uncertainty lingers.

Copper Spikes on Fresh Tariff Fears

Copper markets saw a violent move after President Trump floated a proposal to impose up to 50% tariffs on imports of semiconductors, copper, and pharmaceuticals.

U.S. copper futures surged over 10%, hitting all-time highs, while LME and Shanghai copper contracts lagged behind due to regional trade distortions and logistical constraints. This divergence highlights growing fragmentation in global commodities pricing—a trend to watch if tensions escalate.

Dollar Rises as Trade Anxiety Returns

The U.S. dollar climbed to a two-and-a-half-week high, bolstered by renewed trade protectionism and rising expectations that Friday’s CPI release may remain elevated. While markets didn’t react as sharply as during earlier tariff cycles, sentiment remains cautious—signaling investors may be growing desensitized to trade posturing, at least in the short term.

Global Equities: Divergence Emerges

Equity performance was mixed:

- U.S. indices rose on ETF optimism and tech momentum: S&P 500 +0.7%, Nasdaq +1.2%

- Asian markets split: Japan, Hong Kong, and Australia declined, while South Korea and China posted modest gains.

- European equities opened flat as investors weighed copper supply risks against ECB policy expectations.

What’s Next: CPI & PPI in the Spotlight

Markets now shift focus to Friday’s U.S. CPI and PPI prints, which could confirm or disrupt the current “risk-on” mood.

Consensus sees CPI at 2.9% YoY. A surprise in either direction could reshape ETF flows, interest rate expectations, and currency positioning into next week.

Bottom Line

Crypto is back in focus—and this time, it’s flowing through regulated ETFs with size. Combined with tariff tensions and inflation watch, this midweek marks a turning point where capital rotation and macro positioning are converging fast.

Follow CG FinTech’s Media Center for more Expert Insights!

Forward Looking Statement Disclaimer

This document contains forward-looking statements, which can generally be identified by the words “expects,” “believes,” “continues,” “may,” “estimates,” “anticipates,” “hopes,” “intends,” “plans,” “potential,” “predicts,” “should,” “will,” or similar expressions. Such statements are based on CG FinTech’s current expectations and assumptions, but actual results could differ materially from those anticipated due to a number of risks and uncertainties. CG FinTech does not guarantee the accuracy or completeness of these statements and undertakes no obligation to update or revise any forward-looking statements.

Disclaimer

The information provided herein is for informational purposes only and does not constitute an offer or solicitation to buy or sell any financial instruments. Trading Contracts for Difference (CFDs) and foreign exchange (forex) carries a high level of risk and may not be suitable for all investors. It is important to fully understand the risks involved and seek independent financial advice if necessary.

Leave a Reply