Markets are entering June under the weight of shifting dynamics—economic, political, and structural. From Nvidia overtaking Microsoft to lead the global equity stage, to the European Central Bank easing rates in response to rising trade risks, to OPEC+ reversing its production cuts, the global financial landscape is once again in flux. Meanwhile, mixed manufacturing signals from the U.S. reflect the uncertainty facing real economy sectors.

Nvidia Becomes World’s Most Valuable Company—Despite Export Headwinds

Nvidia’s ascent to a $3.45 trillion market capitalization, surpassing Microsoft, marks a defining moment for the AI-driven rally. The company’s stock gained 3% on June 3, buoyed by continued enthusiasm for its dominance in AI chips and data center infrastructure.

While new U.S. export restrictions to China could dent Nvidia’s revenue by up to $8 billion, investor sentiment appears firmly anchored in the company’s long-term growth potential. This divergence—between near-term geopolitical risk and long-term thematic optimism—illustrates the market’s growing conviction that Nvidia is more than a tech play; it’s a structural growth story in a reshaping global economy.

Markets in Transition: ECB Cuts Rates Again Amid Trump-Driven Trade Risks

On June 5, the European Central Bank reduced its benchmark rate to 2%, marking its eighth cut in the current cycle. The move reflects growing concern over trade uncertainty, particularly stemming from escalating U.S. protectionism under Trump’s evolving tariff policy.

The ECB acknowledged that while the eurozone economy has been relatively resilient to global shocks, the growth outlook has deteriorated. By cutting rates further, the central bank aims to cushion the economy from external headwinds and keep credit conditions supportive across the bloc.

OPEC+ Pivot: From Cuts to Supply Restoration

OPEC+ has signaled a major strategic shift. Beginning in July, eight members—including Saudi Arabia and Russia—will increase output by 411,000 barrels per day, reversing course from prolonged supply cuts.

The move comes amid:

- Weakened pricing power from past cuts

- Rising non-OPEC supply

- Internal disagreements over compliance

- Political pressure from the U.S. to ensure energy affordability

Analysts forecast that the full 2.2 million barrels per day of voluntary cuts may be unwound by September, potentially reshaping the supply side of the oil market through the second half of 2025.

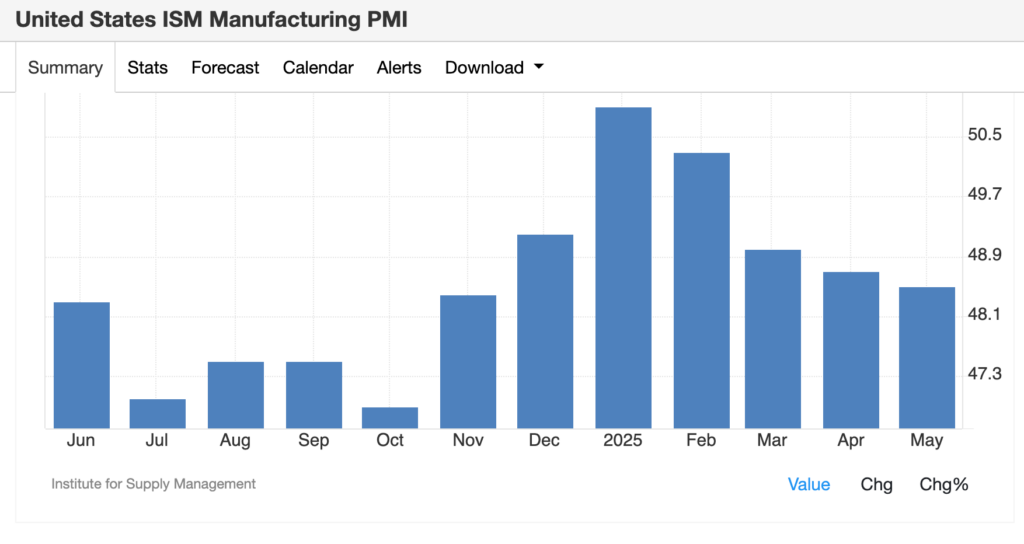

U.S. Manufacturing: Data Divergence Underscores Economic Ambiguity

The latest U.S. manufacturing data presents a confusing picture. The ISM Manufacturing PMI fell to 48.5 in May, signaling contraction for the third straight month. However, S&P Global’s PMI rose to 52.3, suggesting moderate expansion.

This split reflects sectoral differences and varying sample scopes across surveys, but it also highlights the fragile and uneven recovery in U.S. industrial output. As higher interest rates and global trade shifts weigh on demand, the manufacturing sector remains a wildcard in broader economic performance.

Markets in Transition: This Week’s Market Snapshot

As policy shifts and sector developments unfolded, equity markets delivered mixed performance across regions:

- S&P 500: +1.8% Driven by tech gains and cooling inflation data earlier in the week, U.S. equities remained resilient despite rate uncertainty and geopolitical risks.

- Nasdaq Composite: +2.9% Led by Nvidia’s surge and renewed momentum in AI-linked stocks, the Nasdaq outperformed, reclaiming investor confidence in growth sectors.

- Dow Jones Industrial Average: +0.5% Blue chips lagged behind as defensives underperformed and industrials reacted to mixed manufacturing data.

- Stoxx Europe 600: -0.4% European equities dipped slightly, with sentiment weighed by ongoing trade tension spillovers and cautious reactions to the ECB’s latest rate cut.

- Nikkei 225: +1.1% Japan’s market saw modest gains, supported by global tech optimism and a softening yen that boosted export sentiment.

This week’s performance underscores the divergence between growth-oriented U.S. tech and broader global equity sentiment, with central bank policy and trade risks continuing to drive cross-asset rotation.

Stay Informed with CG FinTech’s Media Center

For comprehensive analyses and the latest updates on global financial markets and global developments, follow CG FinTech’s Media Center. Our expert insights aim to equip you with the knowledge to navigate today’s fast-changing landscape.

Forward Looking Statement Disclaimer

This document contains forward-looking statements, which can generally be identified by the words “expects,” “believes,” “continues,” “may,” “estimates,” “anticipates,” “hopes,” “intends,” “plans,” “potential,” “predicts,” “should,” “will,” or similar expressions. Such statements are based on CG FinTech’s current expectations and assumptions, but actual results could differ materially from those anticipated due to a number of risks and uncertainties. CG FinTech does not guarantee the accuracy or completeness of these statements and undertakes no obligation to update or revise any forward-looking statements.

Disclaimer

The information provided herein is for informational purposes only and does not constitute an offer or solicitation to buy or sell any financial instruments. Trading Contracts for Difference (CFDs) and foreign exchange (forex) carries a high level of risk and may not be suitable for all investors. It is important to fully understand the risks involved and seek independent financial advice if necessary.

Leave a Reply