Markets entered the week cautiously optimistic. But by midweek, a harsher tone had taken hold. The trigger? A hotter-than-expected U.S. CPI print, rapidly climbing Treasury yields, and a revived U.S. dollar rally—reminding investors that inflation, though slower, isn’t done reshaping portfolios.

U.S. CPI Surprises: Soft Landing No Longer the Base Case

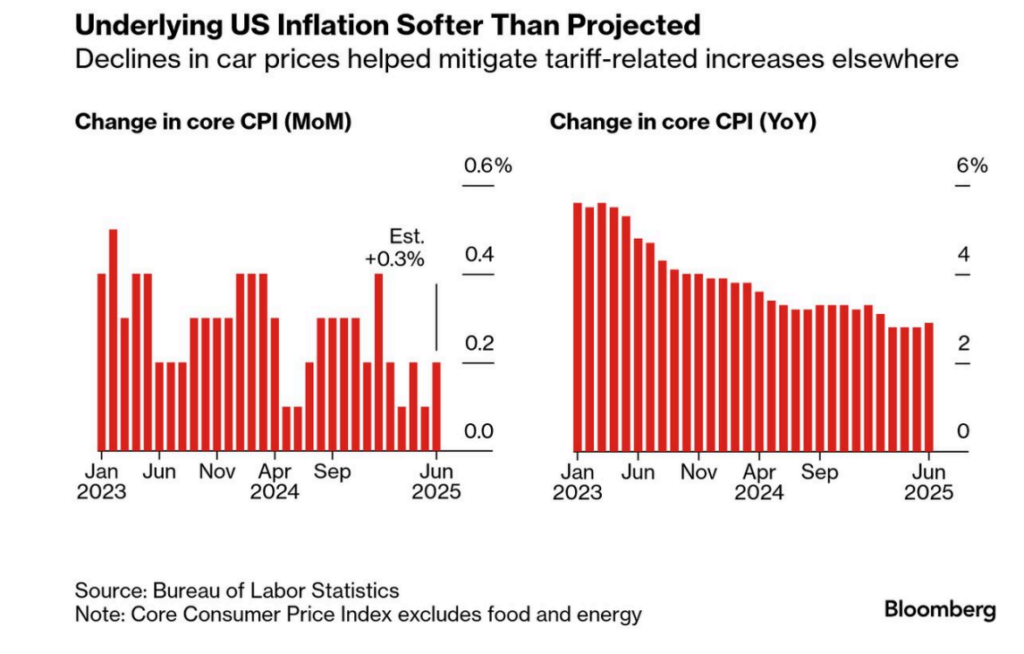

June’s U.S. CPI report came in at +0.3% MoM, higher than expected and the fastest pace since January. While the year-over-year reading held at 2.7%, it’s the monthly acceleration that raised eyebrows. Markets were quick to adjust. Fed rate cut bets were slashed—just one 25 bps cut now priced for 2025, down from nearly two at the start of the month.

Behind the headline number were signs of deeper concern. Shelter inflation showed signs of stickiness, while goods inflation was mildly reaccelerating, potentially due to renewed tariff pressures. The policy risk now isn’t just whether the Fed will cut—it’s whether they’ll be forced to stay on hold into 2026.

Yields Jump Across the Curve: Bond Markets Flash a New Signal

The Treasury curve shifted sharply higher in recent days. The 30-year yield breached 5%, marking a level unseen since early June. Short-term yields spiked in tandem, and the curve steepened—a classic signal of markets repricing the long-term neutral rate upward.

Charts from institutional outlooks show this clearly: the entire U.S. yield curve is lifting, with the front-end leading the move. That’s not just technical noise. It suggests investors are abandoning hopes of a dovish pivot and bracing for longer-lasting inflation pressure—even if growth slows.

Dollar Roars Back: FX Traders Reprice Risks

The U.S. Dollar Index (DXY) surged to a two-month high this week, driven by rising yields and global rate differentials. The Japanese yen and Canadian dollar took the biggest hits, while the euro and pound slipped as well. FX traders are now reevaluating the carry trade environment, especially as the Bank of Japan holds rates steady and offers little forward guidance.

Dollar strength is also weighing on EMFX and commodities—two areas that had been beneficiaries of early-summer softness in the greenback.

Nvidia Pushes Nasdaq Higher—But the Rally Is Narrowing

If there’s one bright spot this week, it’s tech—again. Nvidia shares rose 4%, buoyed by news that U.S. regulators approved additional AI chip exports to China. That move helped push the Nasdaq to another all-time high, but the broader equity rally is losing breath.

While the Nasdaq posted gains, the S&P 500 slipped 0.4% and the Dow dropped 1%, signaling that the tech rally is masking broader market hesitation. Rate-sensitive sectors like REITs and financials led declines. This divergence—between mega-cap tech and the rest of the market—reflects how narrow the path to outperformance has become.

Crypto Resilience Amid Macro Volatility

Even as risk sentiment cooled elsewhere, Bitcoin continued its rebound, briefly touching $123,000 on Tuesday. The driver? Persistent ETF inflows—now over $4 billion this month—and increasing clarity around U.S. crypto legislation.

Ethereum followed, though gains were modest. Interestingly, gold also rose alongside crypto—up 0.5% on the week—suggesting both digital and traditional safe havens are finding demand in an environment that suddenly looks less “soft landing” and more “sticky stagflation.”

What Markets Are Watching Now

The next 48 hours will be critical. The U.S. PPI print is due today, followed by a wave of bank earnings—Goldman Sachs, Morgan Stanley, and Bank of America among them. Together, they’ll offer clarity on both margins and credit risk—two factors the bond market is watching closely.

Add to that rising political risk (from tariffs to BRICS realignment), and it’s clear this midweek isn’t a pause—it’s a pivot.

Conclusion

This week’s price action tells a clear story: inflation isn’t fading fast enough, and markets are rethinking the Fed timeline. With the dollar rising, bonds repricing, and equities starting to fracture, capital is shifting again—out of hope, and into defense.

For daily insights and real-time macro strategy, follow CG FinTech Media Center—where news meets execution.

Forward Looking Statement Disclaimer

This document contains forward-looking statements, which can generally be identified by the words “expects,” “believes,” “continues,” “may,” “estimates,” “anticipates,” “hopes,” “intends,” “plans,” “potential,” “predicts,” “should,” “will,” or similar expressions. Such statements are based on CG FinTech’s current expectations and assumptions, but actual results could differ materially from those anticipated due to a number of risks and uncertainties. CG FinTech does not guarantee the accuracy or completeness of these statements and undertakes no obligation to update or revise any forward-looking statements.

Disclaimer

The information provided herein is for informational purposes only and does not constitute an offer or solicitation to buy or sell any financial instruments. Trading Contracts for Difference (CFDs) and foreign exchange (forex) carries a high level of risk and may not be suitable for all investors. It is important to fully understand the risks involved and seek independent financial advice if necessary.

Leave a Reply