Global markets staged a broad-based rally this week, propelled by a cocktail of positive catalysts: cooling inflation in the U.S., renewed trade diplomacy between the world’s largest economies, and an earnings season that delivered both surprises and warnings. While some asset classes like gold faltered, risk-on sentiment dominated most of the landscape, lifting equities, pressuring the U.S. dollar, and keeping volatility in check.

Equities Climb as Macro Winds Turn Favorable

Equity markets across the globe caught a strong bid, with U.S. indices leading the charge. The S&P 500 surged 5.3% to close at 5,958.38 on Friday, notching five consecutive daily gains and inching closer to its all-time high. The Nasdaq outperformed, soaring 7.2% for the week, underpinned by a fresh wave of enthusiasm in artificial intelligence plays after Nvidia’s upbeat results. The Dow Jones Industrial Average added 3.4%, reflecting strength not only in tech but across financials, industrials, and discretionary sectors.

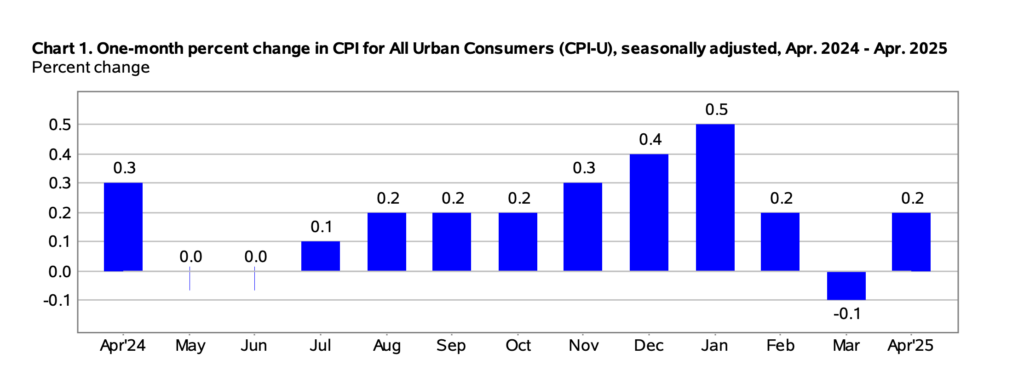

The bullish momentum was driven in part by softer-than-expected U.S. inflation data. April’s Consumer Price Index (CPI) came in at 2.3% year-over-year, the lowest annual increase since February 2021, while month-over-month inflation rose by just 0.2%. Traders interpreted the moderation as a green light for potential rate cuts later this year. By Friday, CME FedWatch data showed a 55% probability of a rate reduction by September—a shift that underpinned both equities and rate-sensitive assets.

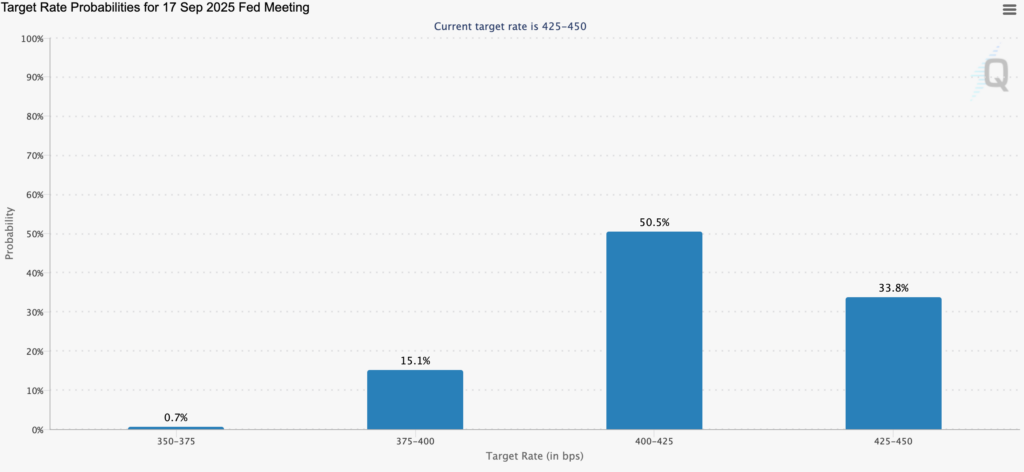

By Friday, CME FedWatch data showed a 50.5% probability of a rate reduction by September—a shift that underpinned both equities and rate-sensitive assets.

Fed Messaging: Cautious, but Market-Led

Despite growing market confidence in a dovish pivot, Fed officials themselves maintained a cautious stance. Speaking Thursday, Fed Chair Jerome Powell acknowledged the downward trend in inflation but reiterated that further progress is needed before any policy changes can be enacted. Several regional Fed presidents echoed similar caution, suggesting any action will remain “data-dependent.”

Still, the disconnect between Fed rhetoric and market pricing has grown more pronounced—a dynamic that will likely shape risk sentiment into the summer.

Trade Truce Sparks Relief Rally

Geopolitical relief also added to the bullish tone. Early in the week, Washington and Beijing jointly announced a 90-day suspension of newly proposed tariffs, opening the door to renewed bilateral trade talks. Investors interpreted the move as a constructive step in de-escalating tensions that have weighed on global supply chains and emerging markets since late 2023.

The truce gave particular support to export-heavy sectors and emerging market assets, while reducing immediate demand for traditional safe havens like gold.

Forex: Dollar Eases, EUR/USD Eyes Breakout

In currencies, the U.S. dollar softened as expectations of looser monetary policy began to take hold. The DXY index fell modestly over the week, while EUR/USD edged toward a key resistance zone at 1.1375. Traders watched the pair carefully for signs of a breakout, though by Friday, price action remained contained within a broader consolidation channel.

From a technical standpoint, the euro remains supported by narrowing interest rate differentials and relative economic stability in the Eurozone, despite flat GDP growth in Q1. Failure to clear the 1.1375 level, however, could expose the pair to a correction back toward the 1.07 region.

Commodities: Gold Breaks Down as Risk Appetite Rises

Gold endured a rough week, slipping to its lowest level in over a month. XAU/USD traded below $3,300 per ounce on Friday, failing to attract safe-haven flows amid easing geopolitical risks and a rebound in equity risk appetite.

Technical pressure added to the decline. The metal broke through multiple support levels, with key downside targets now located near $3,135. Momentum indicators such as the Relative Strength Index (RSI) suggest room for further weakness unless gold can reclaim the $3,280–$3,335 zone. The inverse correlation with real yields and the U.S. dollar will continue to dictate gold’s next leg.

Oil Prices Hold Steady Despite Inventory Surprise

In energy global markets, crude oil remained relatively flat despite a surprise build in U.S. inventories. Brent crude ended the week near $64 per barrel, with WTI following a similar path. The market is caught between two forces: concerns about demand, particularly in Asia, and tightening supply conditions caused by extended production cuts from OPEC+.

Volatility in the oil space has cooled significantly, with traders awaiting clearer signals from both global demand data and the June OPEC meeting.

Corporate Earnings: AI Booms, Retail Cautions

Earnings continued to trickle in, adding nuance to the broader rally. Nvidia reported another blockbuster quarter, reaffirming its dominance in the AI hardware space and sending its stock to new highs. AMD followed suit, benefiting from the same secular trend.

On the flip side, U.S. retail giant Walmart issued a cautious outlook for the second half of 2025, citing persistent cost pressures and early signs of slowing consumer demand. Meanwhile, Alibaba beat revenue forecasts but flagged concerns over weakened sentiment in China’s consumer sector—hinting at lingering domestic fragility despite policy support.

These mixed signals underscore a growing divergence between tech-led optimism and broader economic reality.

Looking Ahead

Next week brings several potential catalysts: flash PMI readings from Europe, minutes from the last FOMC meeting, and Japan’s inflation data. Traders will also closely monitor language from central banks globally as the debate over timing and scope of rate cuts intensifies.

Follow more insights at CG FinTech Media Center – your pulse on global markets.

Forward Looking Statement Disclaimer

This document contains forward-looking statements, which can generally be identified by the words “expects,” “believes,” “continues,” “may,” “estimates,” “anticipates,” “hopes,” “intends,” “plans,” “potential,” “predicts,” “should,” “will,” or similar expressions. Such statements are based on CG FinTech’s current expectations and assumptions, but actual results could differ materially from those anticipated due to a number of risks and uncertainties. CG FinTech does not guarantee the accuracy or completeness of these statements and undertakes no obligation to update or revise any forward-looking statements.

Disclaimer

The information provided herein is for informational purposes only and does not constitute an offer or solicitation to buy or sell any financial instruments. Trading Contracts for Difference (CFDs) and foreign exchange (forex) carries a high level of risk and may not be suitable for all investors. It is important to fully understand the risks involved and seek independent financial advice if necessary.

Leave a Reply